If you’ve recently transitioned from full-time employment to freelancing or contracting, one of the first things you need to get to grips with is self employment tax and social security.

When you worked for an employer, this was all relatively straightforward. Your employer would deduct social security taxes from your paycheck, match your contribution, then send the tax to the Internal Revenue Service (IRS). Simple.

But as a freelancer, the buck stops with you. In this post, we share some vital social security tips and tricks to make your life easier — both now and in the future.

Here are our top 5 social security tips & tricks for freelance workers.

1. To maximize your benefit, work as long as possible

To understand how your social security benefit is calculated, take a look at this information sheet from the SSA. In short, it’s based on your average monthly earnings, adjusted for inflation, and taken over your 35 highest-earning years.

At a minimum, you should aim to work for 35 years. If you work fewer than that, your benefit calculation will be smaller, which, in turn, reduces the size of your checks.

But if you manage to work longer than those 35 years, any low-earning years will be replaced by your higher-earning years. For example, if you’ve just started out in freelancing, you may have a few years of low income as you build your business, skills, and reputation. Ideally, you’ll want to work on longer to ensure those early years are disregarded in your social security calculations.

2. Make sure you’re charging enough for your services

As an extension of tip #1, it’s clear that the more money you make during your 35 years, the higher your social security benefit when you retire.

For those employed by an employer, this can prove challenging, as they’re often left with the choice of either working overtime or taking on an extra job.

But as a freelancer, your earning potential is close to limitless. You can choose how much you charge, which services to offer, and continually upskill to compete in an ever-changing landscape.

Not sure how much you should be charging? Check out our freelance rates explorer.

3. Keep money aside for your taxes — all of your taxes!

As we mentioned at the start of the article, the buck stops with you as a freelancer when it comes to tax. You’re required to file an annual income tax return, and you need to pay your estimated tax bill every quarter.

And in addition to that, you also need to pay self-employment taxes, covering Social Security and Medicare — both of which are withheld from salaried employees by their employers.

Wage-earners also get help with their share of social security and Medicare. Their employers are legally obligated to contribute half. Unfortunately, as a freelancer, you’re on your own, which means it’s crucial that you’re disciplined with the money you earn, keeping enough aside to cover all of your tax.

- If you earn over $400 net (the amount you’ve earned minus expenses), you’re subject to the self-employment tax. This works out as 15.3%, of which 12.4% is social security and 2.9% is Medicare.

- The social security tax applies to your net income up to $137,700 for 2020.

- The Medicare tax doesn’t have an income cap, but once you pass $200,000, it adds another 0.9%.

You can read more on the IRS website.

Social Security tips: tackle tax head-on with Bonsai

When you start freelancing, you soon realize that you need to wear several hats on any given day.

Whether you’re primarily a web designer, copywriter, artist, business consultant, or digital marketer, you also need to be a project manager, customer service rep, and bookkeeper all rolled into one.

The top-performing freelancers grasp this quickly, utilizing freelance software to build a solid business management infrastructure. This allows them to create and send contracts, keep track of projects, invoice clients, and make sure income & expenses are recorded and allocated with ease.

And while there are several platforms each specializing in a particular business function, it makes sense to use an all-in-one solution (to save time and money!). Enter: Bonsai.

Bonsai not only gives you access to a range of important freelance features, such as proposals, contracts, invoices, client CRM, and time tracking; it also boasts Bonsai Tax.

Built exclusively for self-employed workers, Bonsai Tax helps you track expenses, maximize tax write-offs, and estimate quarterly taxes. Save an average of $5,600 per year and avoid any nasty surprises at tax time.

Start your 7-day free trial today.

4. Plan for your annual expenses

You might be one of those lucky few freelancers who enjoy a steady stream of income year-round. But the reality for most is that income varies month to month, or ebbs and flows with the seasons.

With this in mind, it’s important that you plan for any dry spells you may face, and make sure you’re not leaving yourself short when tax time rolls around.

- To do this, calculate your annual expenses and divide the number by 12. This should include all of your freelance overheads (including a salary) plus bills and other expenses in your personal life.

- Once you have a number, use this as your income target for each month. Aim to earn at least this amount to cover your expenses.

- Anything earned over and above this number should be set aside to offset those dry spells.

As a rule, try to live off of 50% of your income, putting anything extra towards savings or paying down debt. Just remember, what you make each month isn’t immediately up for grabs. You — and you alone — need to be disciplined and prepared to plan for the future.

5. It might seem far off, but one day, you will retire — plan now!

There’s an endless list of reasons why people go freelance, but chief among them is an inability (or unwillingness) to find work in a traditional Monday-to-Friday, 9-to-5 setting.

And while this is exciting — being your own boss and setting your own rules and schedules — you mustn’t lose sight of the fact that you, too, will one day retire.

This is where many traditional wage earners have the upper hand. Employers contribute to their employees’ eventual retirement fund, and there’s a greater peace of mind that the future is largely taken care of.

But you don’t have to always think of the short-term as a freelancer. Look at the bigger picture and take steps now to safeguard your retirement. Consider opening an Individual Retirement Account (IRA), or a Simplified Employee Pension (SEP) if you’re structured as an LLC. Both give you the opportunity to set money aside for the future, with varying degrees of tax deductions.

You can learn more about the types of IRAs and SEPs in this guide.

Did you know that you can use Bonsai for bookkeeping? Or that Bonsai can help you be prepared for self-employment tax by providing tax estimates, filling date reminders, and identifying your tax write-offs?

Let's see how that works. First, head to your main Bonsai dashboard and have a close look on the left side - we'll be working with the bookkeeping and taxes sections. First click on "Bookkeeping".

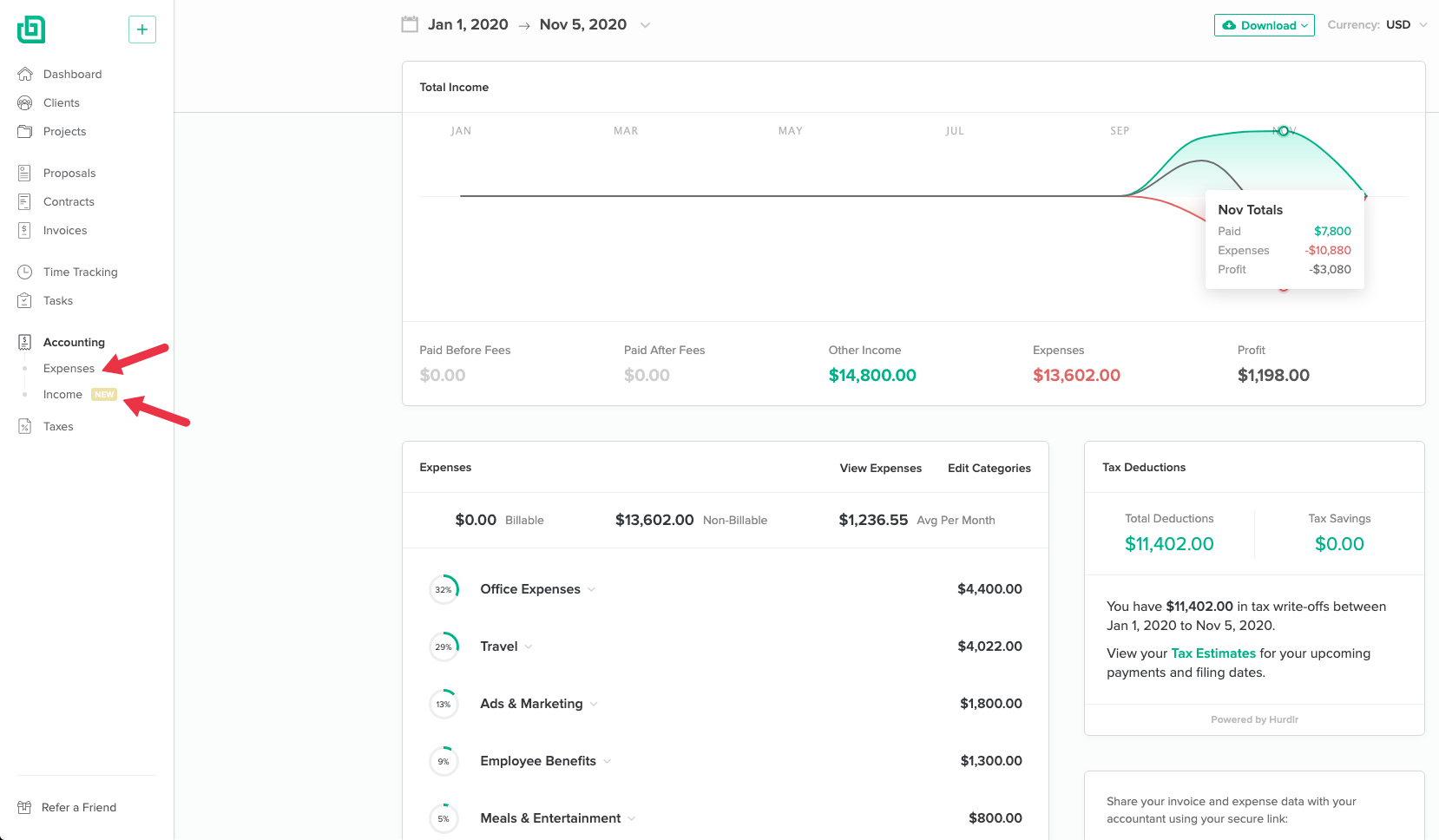

Inside the bookkeeping section, you'll see a breakdown of your income and expenses. Both can either be automatically imported from your bank account, or manually added. Work you got paid for via Bonsai will also be registered here.

Make sure this section is properly filled in and click on "Taxes" next.

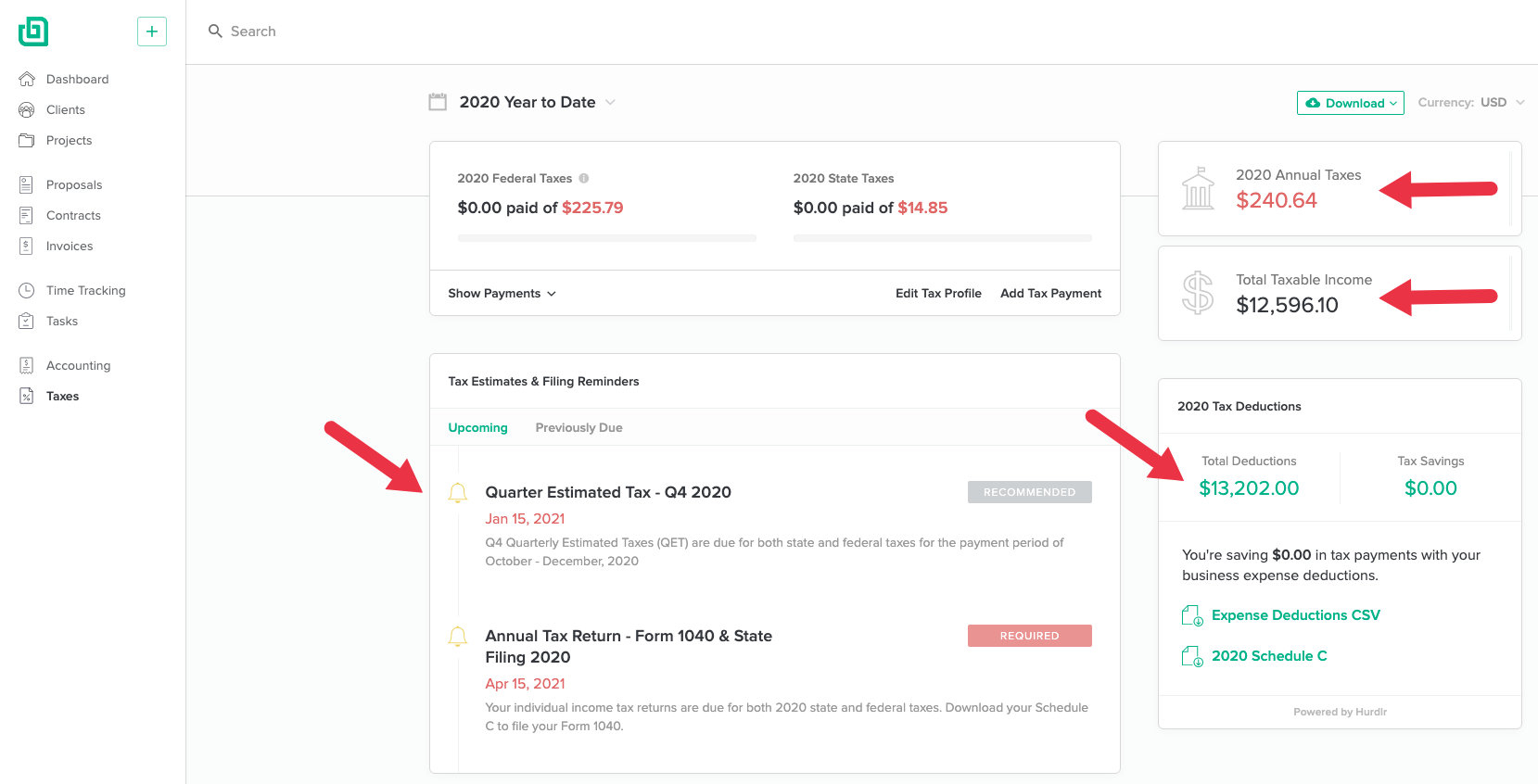

This is where the magic happens: Bonsai taxes will do all the calculations for you, and we'll provide you with an overview of your tax estimates, a list of tax deductions you can use for the upcoming tax season, and reminders for all the upcoming filling dates.

Simple, right? If you're ready to check out Bonsai and explore all the features, go ahead and sign up for the free trial!

In summary

As a freelancer, it’s important that you’re not left to rely solely on your social security checks well into your golden years — especially if you plan on living comfortably, traveling, and looking after loved ones.

Our advice, therefore, is two-fold: First, make sure you’re taking the necessary steps to maximize your contributions now, and second, plan for retirement by setting up a savings account or pension plan.

And, above all else, stay on top of your tax. Use Bonsai Tax to track and automate expenses, maximize write-offs, and estimate your quarterly tax bills.

'%3e%3cg id='Final-Copy-2_2_' transform='translate(1275.000000, 200.000000)'%3e%3cpath class='st0' d='M7.4,12.8h6.8l3.1-11.6H7.4C4.2,1.2,1.6,3.8,1.6,7S4.2,12.8,7.4,12.8z'/%3e%3c/g%3e%3c/g%3e%3c/g%3e%3cg id='final---dec.11-2020'%3e%3cg id='_x30_208-our-toggle' transform='translate(-1275.000000, -200.000000)'%3e%3cg id='Final-Copy-2' transform='translate(1275.000000, 200.000000)'%3e%3cpath class='st1' d='M22.6,0H7.4c-3.9,0-7,3.1-7,7s3.1,7,7,7h15.2c3.9,0,7-3.1,7-7S26.4,0,22.6,0z M1.6,7c0-3.2,2.6-5.8,5.8-5.8 h9.9l-3.1,11.6H7.4C4.2,12.8,1.6,10.2,1.6,7z'/%3e%3cpath id='x' class='st2' d='M24.6,4c0.2,0.2,0.2,0.6,0,0.8l0,0L22.5,7l2.2,2.2c0.2,0.2,0.2,0.6,0,0.8c-0.2,0.2-0.6,0.2-0.8,0 l0,0l-2.2-2.2L19.5,10c-0.2,0.2-0.6,0.2-0.8,0c-0.2-0.2-0.2-0.6,0-0.8l0,0L20.8,7l-2.2-2.2c-0.2-0.2-0.2-0.6,0-0.8 c0.2-0.2,0.6-0.2,0.8,0l0,0l2.2,2.2L23.8,4C24,3.8,24.4,3.8,24.6,4z'/%3e%3cpath id='y' class='st3' d='M12.7,4.1c0.2,0.2,0.3,0.6,0.1,0.8l0,0L8.6,9.8C8.5,9.9,8.4,10,8.3,10c-0.2,0.1-0.5,0.1-0.7-0.1l0,0 L5.4,7.7c-0.2-0.2-0.2-0.6,0-0.8c0.2-0.2,0.6-0.2,0.8,0l0,0L8,8.6l3.8-4.5C12,3.9,12.4,3.9,12.7,4.1z'/%3e%3c/g%3e%3c/g%3e%3c/g%3e%3c/g%3e%3c/svg%3e)