Running an online business is a lot of work. There are so many things to think about – from creating great content to driving traffic to your website, to making sales and fulfilling orders. One thing that you don't want to worry about is your bank account.

The good news is that there are plenty of great business bank accounts out there that can help you manage your finances and save money (all with different bank account requirements).

Here are some of the best business checking accounts for e-commerce:

- Axos

- Relay

- TIAA

- BlueVine

- Mercury

- Chase

Axos Small Business Banking

Axos is the oldest and most well-known online bank in the United States.

The online bank offers two options that may be ideal for e-commerce business owners:

- Axos Basic Business Checking account

- Axos Small Business Interest Checking account

Basic Business Checking has no monthly charges and requires no minimum deposit to open, but you won't earn interest.

The Small Business Interest Checking account, on the other hand, earns interest on your balance, but it requires you to pay a monthly fee. You can, however, qualify to get the fee waived.

With the Basic Business Checking account, you'll receive your first 50 checks for free and up to 200 free transactions (deposits, credits, and debits into the account) each month when you open it. There is a $1,000 minimum deposit requirement, though, which is relatively high compared to other banks.

The Business Interest Checking account has an annual percentage yield (APY) of 0.81% on balances up to $50,000. If you maintain a balance of over $50,000, you can still earn interest, albeit at a lower rate.

With a balance of $50,000 to $250,000, you'll earn an interest of 0.20%. And if you maintain a higher balance ($250,00 40 $5 million), the account will pay out interest of 0.10%.

To open the Business Interest Checking account, you'll have to make a minimum deposit of $100, which is rather modest compared to other bank accounts. Also, if you maintain an average balance of $5,000, you can waive the $10 monthly maintenance fee that the bank charges.

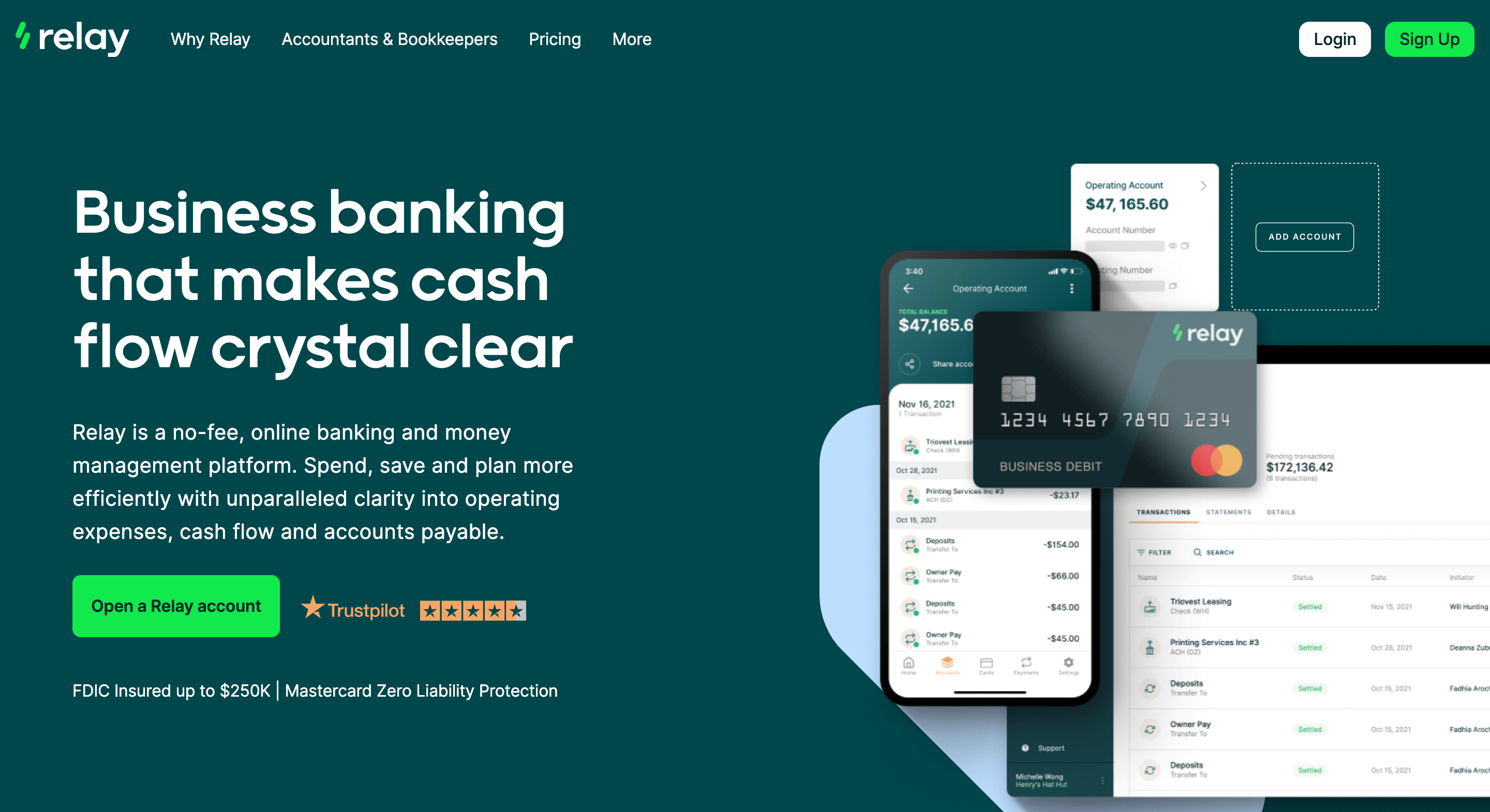

Relay Business Banking

Relay is a fully digital business account service that offers free business checking. There are no minimum balance requirements, transaction limits, or overdraft fees with Relay, and it also includes free incoming wire transfers, as well as the ability to create many accounts.

For $30 a month, you can get access to Relay's premium account, Relay Pro, which provides same-day ACH availability and free outgoing wire transfers, as well as accounts payable features such as the ability to automatically import bills from accounting platforms.

That said, Relay has no physical branches, so all financial transactions are completed on the website or mobile app.

TIAA Small Business Checking Accounts

TIAA's Small Business Checking account – which was designed particularly for sole proprietors and single-owner LLCs – comes with a number of benefits to help you manage your business's finances more effectively.

It’s a 0.10% APY interest-bearing checking account that requires a $1,500 minimum deposit to open. The bank, though, doesn't require you to pay any monthly maintenance fees.

The account balances the benefits of online business account with the convenience of having an ATM machine just around the corner, as it has one of the most extensive ATM networks in the nation.

This account reimburses you for any ATM fees you incur when making withdrawals at an out-of-network machine. The catch, though, is that you need to maintain a balance of at least $5,000 in your account. If you have a balance of $5,000, TIAA will only reimburse you up to $15 every month.

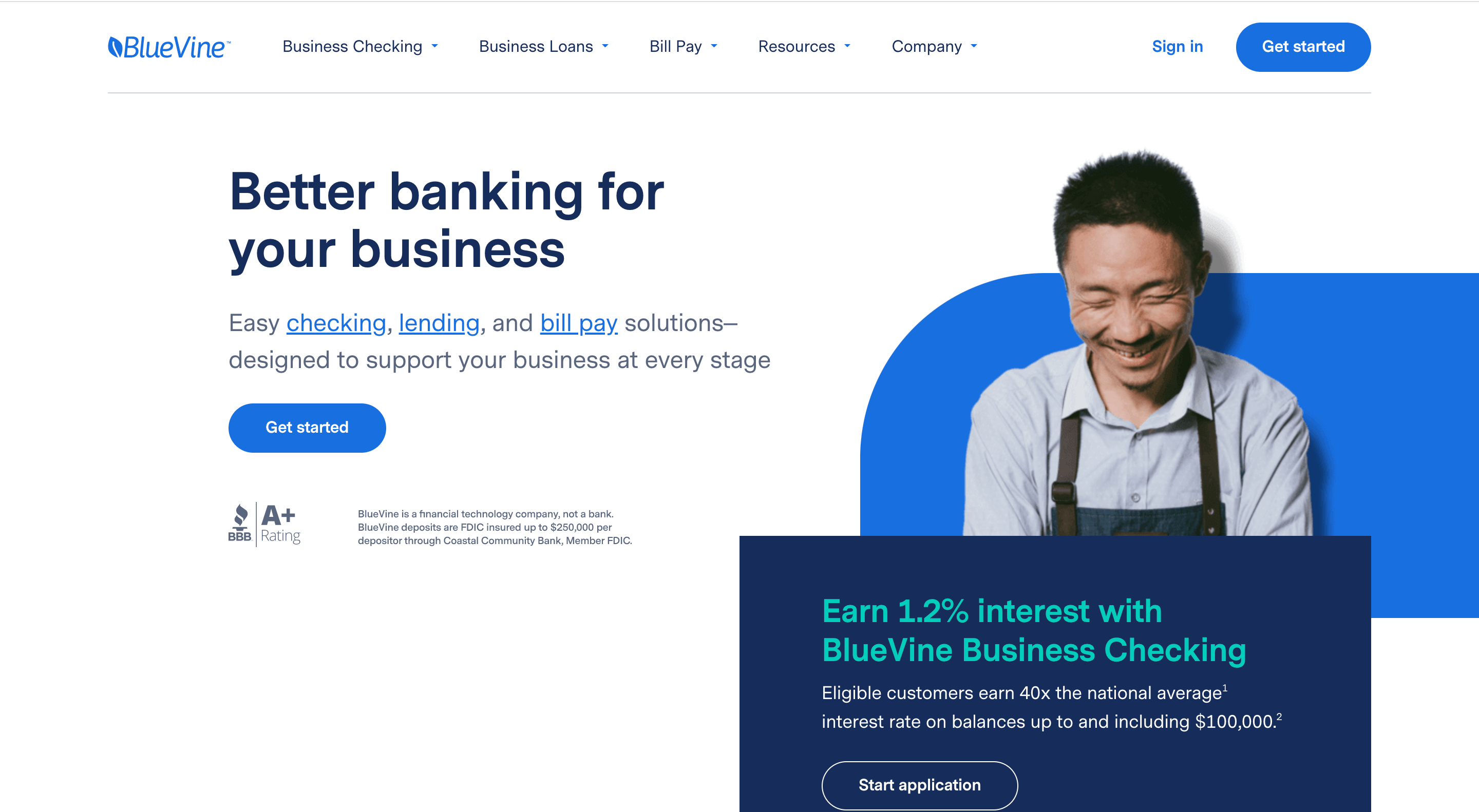

BlueVine Business Checking Accounts

BlueVine is an online-based, FDIC-insured bank that provides its clients with a business checking account as well as a line of credit. Some of BlueVine's most attractive features include:

- Minimal fees

- Revolving credit scheme

- Debit mastercard

- Unlimited transactions

Even with all these features, what makes this account stand out is its high APY. BlueVine offers a 1.2% APY on balances ranging between $1 and $100,000.

Given that the national average for interest checking accounts is 0.03% and savings accounts rates average 0.06%, it's evident that BlueVine's 1.2% interest rate is remarkable and is ideal for most e-commerce business owners.

Mercury

Mercury is an online-only business account platform that requires no monthly service fee, no transaction costs, no minimum deposits, and no minimum balances. To top it off, Mercury provides fee-free access to withdraw cash through the Allpoint network and does not charge for out-of-network ATM usage, although you may be charged by the ATM provider.

You can use the account’s built-in digital tools to send and receive online payments, monitor transactions and cash-flow stats, and track spending. The iOS app from Mercury allows you to manage your debit card — edit spending limitations, freeze it, add it to your mobile wallet — as well as create virtual debit cards through its software.

All in all, Mercury makes it very easy for you to get started with low-cost business account. You can quickly set up a business bank account with little effort. This, combined with Mercury's online tools and user permissions, make the account an appealing choice for many e-commerce small business owners.

Chase Business Complete Banking

If you’re looking for a comprehensive business account solution, Chase Business Complete Banking is a great option. With this account, you’ll get access to business checking, savings, and merchant services.

Chase's entry-level checking account, Chase Business Complete Business Account, offers a $300 bonus to new customers, the most of any account in this list. Aside from a bonus, the Business Complete Business Account combines online, mobile, and in-person business account with a user-friendly digital platform and a vast network of physical offices.

Another standout feature of this account is QuickAccept which allows you to use a mobile card reader or the Chase app to receive payment via debit or credit cards. Even though you might incur some transaction fees, this feature can be a great addition to your e-commerce business.

If you’re looking for a one-stop-shop for all your business banking needs, Chase Business Complete Banking is a great option.

Choosing the right bank for your e-commerce business: 9 things you need to know

Taking the time to do your research when looking for an ideal business bank account can help you avoid many headaches down the road.

That said, there are a lot of factors to consider when choosing a bank account for your business, but these eight things are a good place to start.

What’s the process for opening an account?

There are a lot of business account options for new business accounts. The process of opening an account can be time-consuming with traditional banks. You will need to provide the bank with a lot of documentation, and the bank will also likely run a credit check on you and your business which can take a couple of days.

Luckily for you, online banks offer a much simpler and more streamlined process. All you need is your basic information and to be able to link your checking account to the new account.

In terms of time, it should only take a few minutes to open an online account as opposed to days or weeks with a traditional bank. This is a huge benefit for business owners who need to move fast.

What incentives does the bank offer?

While most banks will offer some type of incentive to open an account, it’s important to consider what exactly they are offering and if it’s something your business can actually use.

For example, a bank may offer a sign-up bonus in the form of cash back or points. But if you don’t use the bank’s credit card, then that perk is essentially useless to you.

It’s also important to read the fine print on any incentives offered. There may be restrictions or requirements that make it difficult to actually receive the bonus.

You should also find out if the bank offers any discounts on services that your business uses. For example, some banks will offer discounts on PayPal or Square processing fees.

What are your business cash flow requirements?

This is an important consideration, especially for e-commerce businesses that have a lot of transactions or high sales volumes.

You will want to find a bank that can handle your account without charging you extra fees. To do this, you will need to find out the average monthly balance requirements and the fees charged if you go below that amount.

You will also want to find out what the bank’s policy is on holds and how long they last. This can be a problem if you need access to your funds right away.

What are the fees associated with the account?

Banks make money by charging fees—it’s how they stay in business. But some banks are more fee-heavy than others.

When you’re evaluating different banks, make sure to ask about all the fees to open a bank account or what they charge—including monthly maintenance fees, minimum balance fees, transaction fees, ATM fees, etc.

You should also find out if there are any ways to avoid these fees. For example, some banks waive monthly maintenance fees if you maintain a certain balance in your account.

It’s also important to find out if there are any hidden fees not listed on the bank’s website. The best way to do this is to talk to a representative and ask about all of the potential fees you may be charged.

By getting a full understanding of all the fees you’ll be charged, you can avoid some nasty surprises down the road.

What is their customer service like?

You should be able to count on your bank for help when you need it. After all, they’re handling your money.

In your search for a suitable account, try to find out what a bank’s customer service is like. See if you can get in touch with a representative easily and see how long it takes for them to respond to your inquiry. Some banks only offer phone support, while others also have email and live chat.

Find out what the customer service hours are for the bank you’re considering. Ideally, they should offer 24/seven customer support.

How long does the loan process take?

You should be able to get a loan from your bank without any hassles. After all, that’s one of the primary reasons you have a business account, right?

Look for banks that have an easy and fast loan application process with minimum documentation. Also, inquire about the interest rates and repayment options in advance.

It would be helpful if the bank offers pre-approved loans, so you know exactly how much you can borrow and at what interest rate before you even apply.

Is your bank small business-friendly?

Banks are not all the same when it comes to how they treat small businesses.

Some banks offer special products and services for small businesses while others make it difficult for small businesses to open an account.

You should find a bank that understands your needs as a small business owner and offers products and services that can help you grow your business.

Here are a few things to look for:

- A dedicated small business banker or team of bankers

- Small business products and services, such as loans, lines of credit, and merchant services

- Educational resources, such as seminars and webinars on topics like cash flow management and marketing

Also, note that banks have different areas of expertise, so it’s important to find one that has experience working with businesses like yours.

For example, for an e-commerce business, you might want to consider a bank that has prior experience with online businesses and is comfortable working with the unique needs of an e-commerce business, such as merchant services and payment processing.

You can check this by reading reviews or asking for referrals from other business owners.

Does the bank offer online and mobile banking?

In today’s digital world, it’s important that your bank offers mobile and online banking.

Mobile and online business account allow you to do your business account from the comfort of your home or office—or even on the go.

Mobile and online business account features may include:

- Transferring funds between accounts

- Paying bills

- Viewing account balances and transactions

- Managing account alerts

Some banks have more user-friendly platforms than others. When you’re evaluating different banks, take some time to test out their online banking platforms. See how easy it is to use and navigate.

What’s the minimum balance requirement?

A minimum balance is the least amount of money that you are required to keep in your account by your bank. If at any time, your account falls below this limit, the bank may charge you a fee.

For example, let’s say the minimum balance requirement for your business checking account is $500. If your account balance falls below $500 at any point in time, the bank may charge you a fee of $25.

It’s important to understand the minimum balance requirements of the bank before making a decision.

Final Thoughts For Business Checking Accounts

E-commerce businesses have different needs than traditional brick-and-mortar businesses, so it’s important to find a bank that understands those needs. The right bank will help you grow your business and avoid costly mistakes. Do your research and ask around before making a decision – it’s worth taking the time to get it right.

'%3e%3cg id='Final-Copy-2_2_' transform='translate(1275.000000, 200.000000)'%3e%3cpath class='st0' d='M7.4,12.8h6.8l3.1-11.6H7.4C4.2,1.2,1.6,3.8,1.6,7S4.2,12.8,7.4,12.8z'/%3e%3c/g%3e%3c/g%3e%3c/g%3e%3cg id='final---dec.11-2020'%3e%3cg id='_x30_208-our-toggle' transform='translate(-1275.000000, -200.000000)'%3e%3cg id='Final-Copy-2' transform='translate(1275.000000, 200.000000)'%3e%3cpath class='st1' d='M22.6,0H7.4c-3.9,0-7,3.1-7,7s3.1,7,7,7h15.2c3.9,0,7-3.1,7-7S26.4,0,22.6,0z M1.6,7c0-3.2,2.6-5.8,5.8-5.8 h9.9l-3.1,11.6H7.4C4.2,12.8,1.6,10.2,1.6,7z'/%3e%3cpath id='x' class='st2' d='M24.6,4c0.2,0.2,0.2,0.6,0,0.8l0,0L22.5,7l2.2,2.2c0.2,0.2,0.2,0.6,0,0.8c-0.2,0.2-0.6,0.2-0.8,0 l0,0l-2.2-2.2L19.5,10c-0.2,0.2-0.6,0.2-0.8,0c-0.2-0.2-0.2-0.6,0-0.8l0,0L20.8,7l-2.2-2.2c-0.2-0.2-0.2-0.6,0-0.8 c0.2-0.2,0.6-0.2,0.8,0l0,0l2.2,2.2L23.8,4C24,3.8,24.4,3.8,24.6,4z'/%3e%3cpath id='y' class='st3' d='M12.7,4.1c0.2,0.2,0.3,0.6,0.1,0.8l0,0L8.6,9.8C8.5,9.9,8.4,10,8.3,10c-0.2,0.1-0.5,0.1-0.7-0.1l0,0 L5.4,7.7c-0.2-0.2-0.2-0.6,0-0.8c0.2-0.2,0.6-0.2,0.8,0l0,0L8,8.6l3.8-4.5C12,3.9,12.4,3.9,12.7,4.1z'/%3e%3c/g%3e%3c/g%3e%3c/g%3e%3c/g%3e%3c/svg%3e)