If you are a 1099 truck driver, you need to file your taxes at the end of the year. The IRS considers you self-employed. Being a freelance truck driver carries more responsibility than being a company driver. As a freelancer, you must pay self-employment taxes, record business receipts for deductions, file quarterly tax payments, and more.

This article covers the taxes you owe, the difference between company drivers and freelancers, estimated tax payments, deductions you qualify for, and why Bonsai Tax is the best tax software for truck drivers. Let's begin with the tax forms you'll receive as a self-employed worker.

Note: If you want an easy way to manage your taxes and deductions, try Bonsai Tax. Our software estimates tax liability, sends important filing reminders, scans your credit card/bank receipts, and discovers potential tax write-offs at the push of a button. Users generally save $5,600 from their tax bills. Claim your 7-day free trial today.

What tax forms do you receive as a freelance truck driver?

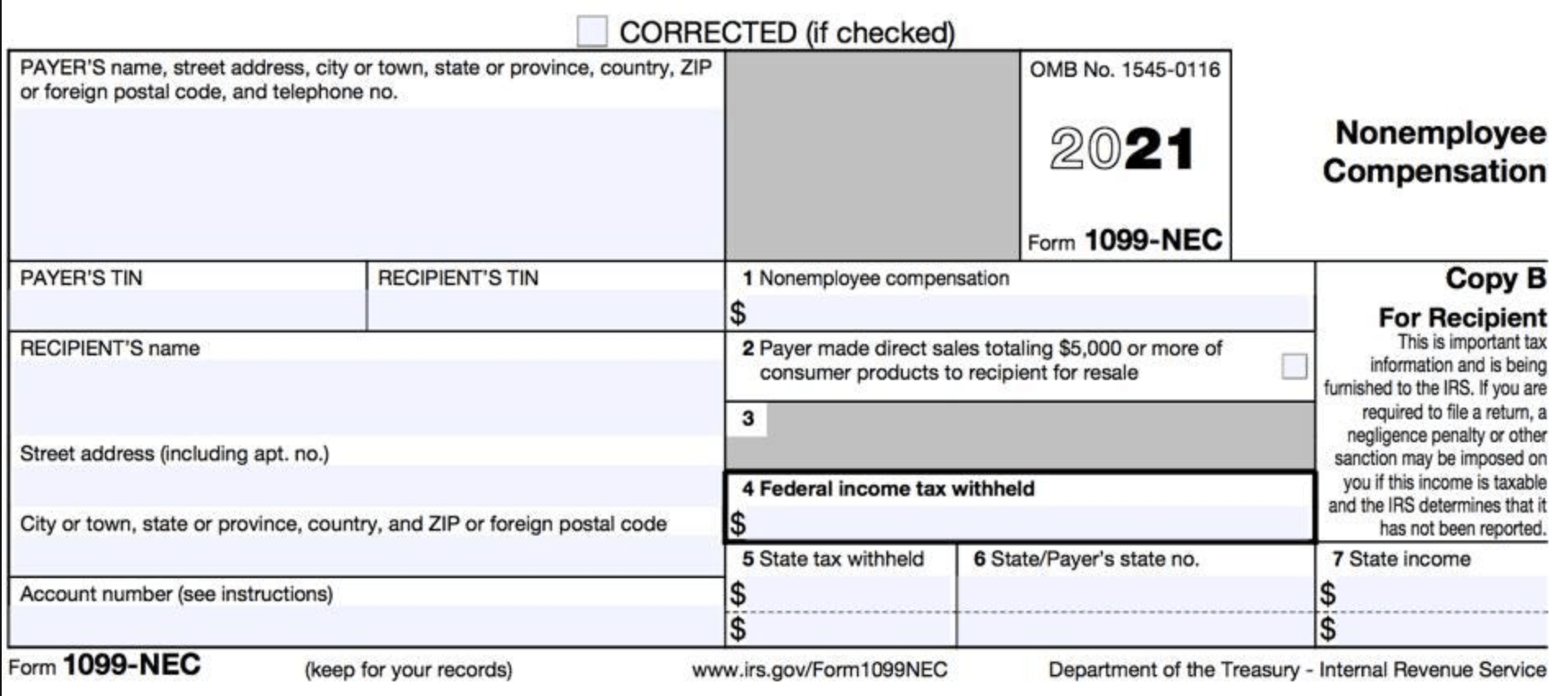

The IRS requires businesses to send freelancers a 1099 form. A 1099 tax form records payments made by a company to freelancers for their services. There are many variations of 1099 forms. The 1099-NEC is the most relevant to you as a 1099 trucking contractor.

Requirements to receive a 1099-nec

The 1099-NEC is the most common tax form sent to independent contractors because of the low threshold to receive it. You get a 1099-NEC if you were paid at least $600 by a business in non-employee payments during the year. Before 2020, the 1099-MISC reported non-employee compensation. The IRS changed these requirements to use the 1099-NEC. As a freelance truck driver, this is your primary tax form.

What to do if you do not receive a 1099?

Businesses must send 1099 forms by January 31. If you freelanced and didn't receive one, there are a few possible reasons. Companies only send a 1099-NEC if they paid you at least $600. If you earned less, they are not required to send a form. You still must report all earnings to the IRS.

You must report all money earned to the IRS. You only avoid self-employment taxes if you make less than $400. However, you remain responsible for paying these taxes. For example, if you earned $500 from freelance truck driving, you won’t receive a 1099. You still need to report the income and pay self-employment taxes.

If you earned over $600 and you did not receive a 1099, check with your client. The address they have on file may be wrong and it was mailed to the wrong place or perhaps they simply forgot. Check in with them to make sure.

How much tax do owner operator truck drivers pay?

As a self-employed worker, you pay self-employment taxes totaling 15.3%. This includes 12.4% for Social Security and 2.9% for Medicare.

To quickly calculate your tax liability, try Bonsai's freelancer tax calculator.

Luckily, you can lower your tax liability by claiming tax deductions for your business. We'll go over recording business receipts and what tax deductions you qualify for later in the article (you'll use a Schedule C).

The minimum income to file self-employment taxes is $400. For example, if you earned $5,000 as a freelancer but had $4,700 in expenses, your net income is $300. You would not owe any self-employment taxes in this case.

As a freelancer, you'll need to file quarterly tax payments four times throughout the year.

We'll go over the due dates and what quarterly taxes are in the next section.

Hidden costs of using 1099 independent contractors in trucking

Increased insurance and liability expenses

Using 1099 independent contractors in trucking often leads to higher insurance and liability costs. Unlike employees, contractors typically carry their own insurance, but many small trucking contractors either underinsure or lack adequate coverage. This gap can leave the hiring company exposed to financial risk if an accident occurs.

For example, a trucking company might pay $1,500 annually for a contractor’s commercial auto insurance, but if that contractor’s coverage is insufficient, the company may face lawsuits or claims that exceed those limits. Additionally, companies might need to purchase additional liability or contingent coverage, which can add thousands of dollars per year.

To manage these risks, businesses should require proof of insurance with specific minimum coverage amounts and consider working with insurance brokers who specialize in trucking. This proactive step helps avoid unexpected costs and legal exposure in 2024 and beyond.

Compliance and misclassification penalties

Misclassifying truckers as 1099 independent contractors rather than employees can result in costly penalties. The IRS and Department of Labor have increased enforcement actions in 2024, with fines reaching up to $5,000 per misclassified worker plus back taxes and benefits owed.

For instance, if a trucking company uses 20 contractors incorrectly classified, it could face penalties exceeding $100,000, not including interest and legal fees. States like California and New York have stricter ABC tests for classification, increasing the risk of audits and fines.

To avoid these penalties, companies should conduct regular classification audits using tools like the IRS’s SS-8 form or consult legal experts specializing in labor law. Clear contracts and documented control levels over work can also help demonstrate proper classification.

Administrative and operational inefficiencies

Relying on 1099 contractors can introduce hidden administrative costs that reduce overall efficiency. Managing multiple independent contractors requires more paperwork, such as issuing 1099 forms, tracking payments, and verifying contractor status, which often demands dedicated administrative time or software.

Operationally, contractors may have varying availability and commitment levels, leading to scheduling challenges and potential delays. Unlike employees, contractors are free to work for competitors, which can disrupt consistent service and customer satisfaction.

Using platforms like QuickBooks Self-Employed or HelloBonsai can streamline contractor payments and tax form management in 2024. Additionally, setting clear expectations and maintaining open communication helps mitigate operational disruptions caused by independent contractors.

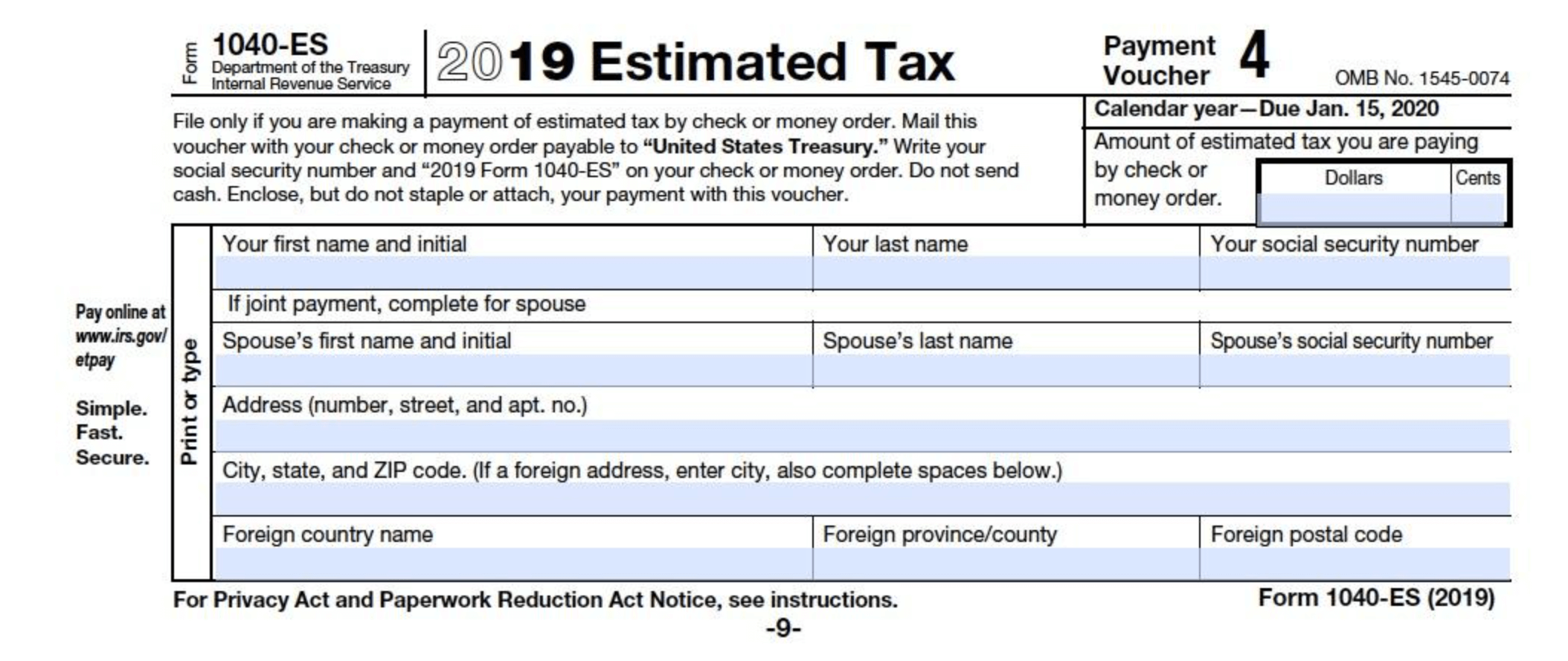

How to file truck driver quarterly taxes

The U.S. runs on a pay-as-you-go system for taxes. You must send estimated taxes throughout the year. These four tax payments, made every three months, cover Social Security, Medicare, and your income tax.

To calculate your quarterly tax payments, all you need to do is add up your total tax liability for the year (including self-employment tax, income tax, and any other taxes) and divide that number by four. This is the amount you'll send to the IRS every quarter. You could also figure out how much you'll pay by using a 1040-ES.

Owner operator due dates for quarterly taxes

The due dates for quarterly taxes in 2024 are:

- April 15, 2024

- June 17, 2024

- September 16, 2024

- January 15, 2026

- April 15

- June 15

- September 15

- January 15 of the following year

You'll need to send in these payments before the due date. Be sure to mark your calendars with the dates so you don't forget and be sure to send in the right amount or you can face a quarterly tax penalty.

You'll be able to send payments directly to the IRS by using Direct Pay.

Read our quick guide to filling estimated tax payments here.

1099 trucking independent contractor tax deductions you qualify for

Let's remove a list of tax deductions available to truck drivers.

Business meal deduction

While most companies are allowed to deduct 50% of lunch meal costs, drivers who are subject to the Department of Transportation's "hours of service" regulations can claim up to 80% of their actual meal costs. The hours of service law compels drivers who have driven a specific number of hours to come to a complete stop and rest for a set amount of time.

Truck drivers are supposed to stop and rest after a specific set of times. They can opt to take the per diem allowance rates. The per diem method is much easier. Instead of keeping track of expenses for every meal, you can deduct a set amount per day. Check Publication 1542 for the Per Diem allowance rates.

Insurance

You can deduct the cost of commercial auto liability, property damage, and health insurance premiums from your tax liability. You may also deduct insurance to cover cargo or lost earnings due to a business interruption.

Tools

The cost of any equipment or tools you need for your trucking business are deductible expenses, including:

- Chains

- Ratchet straps

- Tarps

- Bungee cords

- Duct tape

- Tire irons

Travel expenses

Expenses incurred while you’re away from your "tax home" overnight are deductible. This also includes expenses when you travel long enough to require rest. Deductible costs include:

- Hotels

- Airbnbs

- Tolls

- Parking

Personal products

There are many tax deductions for personal products for owner-operators. These expenses include:

- Cooler or mini fridge to store food and water

- Logbook

- Cleaning supplies

- Flashlight

- GPS

- Sunglasses

- Alarm clock

- Bedding expenses

- Gloves

Traditional office expenses could also be written off.

Vehicle expenses

The IRS classifies a semi-truck as a qualified non-personal-use vehicle. This means you can claim all the actual operating expenses, including:

- Depreciation

- Insurance

- Fuel

- Replacement tires

- Registration fees

- Repair and maintenance costs

- Truck washes

Training and education expenses

In the trucking business, specific training is required to start your career. Applicants applying for a Class A CDL must obtain 30 hours of driving experience from a training school that meets FMCSA standards. This includes at least 10 hours of driving a truck on a practice driving range. The cost of CDL training materials and courses can be deducted.

Software

Read here for our full list of tax deductions for truck drivers.

Note: if you want an easy way to track your trucking deductions, then try Bonsai Tax. Our app will scan your receipts from your bank/credit card statements to discover tax write-offs and maximize deductions. In fact, users save, on average, $5,600 from their tax bill. Try a 7-day free trial here.

Legal risks and consequences of misclassifying truck drivers as independent contractors

Understanding the legal definition of independent contractors versus employees

Misclassifying truck drivers as independent contractors instead of employees can lead to serious legal trouble. The IRS and Department of Labor use strict criteria to determine worker status, focusing on control, financial relationship, and the nature of the work. For example, if a trucking company dictates drivers’ schedules, routes, or requires exclusive use of company trucks, those drivers are likely employees rather than independent contractors.

In 2024, the IRS continues to apply the "Common Law Test" and the "20-Factor Test" to assess classification. Trucking companies must carefully evaluate if drivers operate their own business independently or are integrated into the company’s daily operations. Misclassification often occurs when companies try to save on payroll taxes and benefits but overlook these legal standards.

To avoid misclassification, trucking businesses should document contracts clearly, allow drivers to work for multiple clients, and avoid controlling how drivers perform their work. Consulting legal experts or using classification tools like the IRS’s Form SS-8 can provide clarity before finalizing driver status.

Financial penalties and back taxes from misclassification

Misclassifying truck drivers can trigger significant financial penalties, including back taxes, interest, and fines. The IRS can impose penalties up to 100% of the employment taxes owed if it determines the misclassification was intentional. For 2024, the employer portion of Social Security and Medicare taxes alone can total 7.65% per misclassified driver’s wages, plus federal and state unemployment taxes.

In addition to federal taxes, many states like California and New York have their own strict laws and penalties for misclassification under laws such as California’s AB5. These states may require trucking companies to pay unpaid state payroll taxes and provide benefits retroactively. For example, California’s Labor Commissioner can order payment of wages, overtime, and penalties if drivers are wrongly classified.

To mitigate risks, trucking companies should conduct regular audits of driver classifications and maintain clear records of contracts and work arrangements. Using payroll services like Gusto or QuickBooks Payroll can help track proper tax withholdings and avoid costly mistakes.

Impact on truck drivers and business reputation

Misclassification not only affects companies but also harms truck drivers. Drivers classified as independent contractors miss out on benefits like workers’ compensation, unemployment insurance, and overtime pay. This can lead to disputes and lawsuits that damage the company’s reputation and increase legal costs.

In 2024, several high-profile trucking firms faced class-action lawsuits from drivers seeking reclassification and unpaid benefits. These legal battles often attract media attention, discouraging potential drivers and clients from working with the company. Maintaining proper classification helps foster trust and long-term relationships with drivers.

Trucking businesses should educate drivers about their classification status and provide clear contracts outlining rights and responsibilities. Proactively addressing classification issues reduces legal exposure and supports a positive company culture that attracts quality drivers.

Risk management and insurance considerations for 1099 trucking contractors

Understanding insurance requirements for 1099 trucking contractors

1099 trucking contractors must secure the proper insurance to protect themselves and comply with federal and state regulations. Unlike company drivers, independent contractors are responsible for obtaining their own coverage, including liability, cargo, and physical damage insurance. For example, the Federal Motor Carrier Safety Administration (FMCSA) requires a minimum of $750,000 in liability insurance for most trucking operations, but some states or clients may demand higher limits.

Many contractors choose to purchase insurance through brokers specializing in trucking, such as Progressive Commercial or Great West Casualty Company. These providers offer tailored policies that cover risks unique to owner-operators, including uninsured motorist coverage and non-trucking liability. Contractors should also verify if their contracts specify insurance minimums or require additional endorsements.

To manage costs, consider bundling policies or increasing deductibles where feasible. Regularly reviewing your insurance coverage annually or after major changes in your operation ensures you remain compliant and adequately protected. Taking these steps helps avoid costly gaps in coverage that could jeopardize your business.

Implementing risk management strategies to reduce liability

Effective risk management helps 1099 trucking contractors minimize accidents and liability claims. Start by maintaining a rigorous vehicle inspection routine, documenting all maintenance and repairs. Tools like Fleetio or KeepTruckin can simplify tracking your truck’s condition and service history, reducing the risk of breakdowns or safety violations.

Driver behavior also plays a critical role in risk reduction. Using electronic logging devices (ELDs) mandated by FMCSA helps ensure compliance with hours-of-service rules, preventing fatigue-related incidents. Additionally, adopting defensive driving training programs tailored for truckers can improve safety and lower insurance premiums over time.

Another key strategy is to carefully vet and document all contracts and loads. Avoid high-risk freight or clients with poor payment histories. Using contract management software like HelloBonsai can help you store agreements securely and track important deadlines, reducing disputes and potential legal exposure.

Handling claims and protecting your business assets

When accidents or incidents occur, prompt and organized claims handling is essential for 1099 trucking contractors. Immediately notify your insurance provider and document the event thoroughly with photos, police reports, and witness statements. This evidence supports your claim and speeds up the resolution process.

Separating personal and business assets by establishing a legal business entity, such as an LLC, can protect your personal finances if a claim exceeds your insurance limits. Many states offer relatively low-cost LLC formation services, and platforms like LegalZoom or Rocket Lawyer can assist with setup and compliance.

Finally, consider investing in umbrella insurance policies that provide additional liability coverage beyond your primary policies. This extra layer can be crucial in catastrophic events, safeguarding your long-term financial stability and allowing you to continue operating your trucking business with confidence.

1099 trucking company driver versus independent contractor

Most trucking companies have an employment contract with their workers that outlines the specific classification of their workers. This signed classification is important in regards to tax implications with the IRS. A W-2 employee or an independent contractor is taxed differently. A lot of truck drivers are mislabeled as a freelancer instead of an employee.

As a 1099 worker and not a W-2 employee, you are not considered a fleet employee. There are many key differences between employees and freelance drivers. Here are some of the differences:

- Tax withholding and reporting requirements

- Eligibility for benefits like workers' compensation and unemployment insurance

- Control over work schedules and routes

- Access to company-provided equipment and maintenance

- Legal responsibilities and liabilities

Tax withholding

As a freelance truck driver, you won't have payments withheld by your employer to pay your Federal income tax. On the other hand, employers need to withhold payments to employees in order to cover those. A company driver uses Form W-4 to figure how much money would need to be withheld.

Number of clients

An employee essentially works for the company. Typically, employees work for a single company. A freelancer is independent and can take on a number of clients at a time.

Project timeline

A freelancer, unless contracted for a long duration, generally is used for shorter projects. An employee is used to fill a specific role and for a long duration.

Benefits

An employer typically provides employees with benefits such as:

- Vacation days

- Health insurance

- Dental and vision coverage

- Unemployment insurance

- Life insurance

- Retirement planning

A freelancer does not receive any benefits from their clients.

Time schedule or hours of service

As an employee, your employer can control the hours of service for when you work. As an independent truck driver, you determine when you work.

Control of work completed

Clients cannot control how the work is completed if you are a freelancer. Independent truck drivers' work is governed by project contracts and there are some limits on the control, however, you have complete control over how the work is done.

Tax deductions

Independent truck drivers can leverage 1099 tax deductions to lower their tax liability. Employees are generally reimbursed for costs incurred while working.

ABC test

To determine if a worker is an employee of an independent contractor, many States use the "ABC test". The ABC test is a legal litmus test to determine.

The “ABC test” is a legal test used by many states in employment-related laws, such as for workers' compensation or unemployment compensation, to determine whether a worker is an employee or independent contractor. Many companies try to save money on paying for benefits such as unemployment or medical coverage by claiming workers as freelancers. This test helps mitigate independent contractors from being taken advantage of.

The three rules

According to the Internal Revenue Service, any person providing assistance is considered an employee, not an independent contractor, unless the following conditions are met:

- The individual is free from control and direction in connection with the performance of the service

- The service is performed outside the employer's usual course of business

- The individual is customarily engaged in an independently established trade, occupation, profession, or business of the same nature as that involved in the service performed.

These guidelines will determine if you are an independent contractor or an employee. The trucking industry is notorious for trying to control its workers. Many trucking companies would not pass the ABC test as they tend to exert too much control over the truck drivers.

Bonsai tax helps truck drivers save money

At the end of the year, avoid being stuck with a large tax bill. Take advantage of the benefits of being a self-employed worker and claim all your tax deductions. Bonsai Tax can help you estimate your tax bill, send important tax date reminders, and track all your expenses to lower your tax bill.

Claim your 7-day free trial here.

'%3e%3cg id='Final-Copy-2_2_' transform='translate(1275.000000, 200.000000)'%3e%3cpath class='st0' d='M7.4,12.8h6.8l3.1-11.6H7.4C4.2,1.2,1.6,3.8,1.6,7S4.2,12.8,7.4,12.8z'/%3e%3c/g%3e%3c/g%3e%3c/g%3e%3cg id='final---dec.11-2020'%3e%3cg id='_x30_208-our-toggle' transform='translate(-1275.000000, -200.000000)'%3e%3cg id='Final-Copy-2' transform='translate(1275.000000, 200.000000)'%3e%3cpath class='st1' d='M22.6,0H7.4c-3.9,0-7,3.1-7,7s3.1,7,7,7h15.2c3.9,0,7-3.1,7-7S26.4,0,22.6,0z M1.6,7c0-3.2,2.6-5.8,5.8-5.8 h9.9l-3.1,11.6H7.4C4.2,12.8,1.6,10.2,1.6,7z'/%3e%3cpath id='x' class='st2' d='M24.6,4c0.2,0.2,0.2,0.6,0,0.8l0,0L22.5,7l2.2,2.2c0.2,0.2,0.2,0.6,0,0.8c-0.2,0.2-0.6,0.2-0.8,0 l0,0l-2.2-2.2L19.5,10c-0.2,0.2-0.6,0.2-0.8,0c-0.2-0.2-0.2-0.6,0-0.8l0,0L20.8,7l-2.2-2.2c-0.2-0.2-0.2-0.6,0-0.8 c0.2-0.2,0.6-0.2,0.8,0l0,0l2.2,2.2L23.8,4C24,3.8,24.4,3.8,24.6,4z'/%3e%3cpath id='y' class='st3' d='M12.7,4.1c0.2,0.2,0.3,0.6,0.1,0.8l0,0L8.6,9.8C8.5,9.9,8.4,10,8.3,10c-0.2,0.1-0.5,0.1-0.7-0.1l0,0 L5.4,7.7c-0.2-0.2-0.2-0.6,0-0.8c0.2-0.2,0.6-0.2,0.8,0l0,0L8,8.6l3.8-4.5C12,3.9,12.4,3.9,12.7,4.1z'/%3e%3c/g%3e%3c/g%3e%3c/g%3e%3c/g%3e%3c/svg%3e)